Finance Workers Fear the AI Layoff. The Numbers Disagree.

At the coffee machine in offices or cafeteria tables, you might hear anxious workers whispering about the same fear: AI is coming for their jobs. Some even talk about a superintelligence wiping up all positions within weeks.

The headlines in 2026 are feeding the fear. In March, investment banking giant Morgan Stanley laid off 2,500 employees across all divisions, 3% of its workforce, people familiar with the matter told Bloomberg and Reuters.

The same month, the global investment bank Citigroup announced 265 job cuts by May, with a target of 20,000 by 2026, according to notices filed with the Department of Labor. The CFO Mark Mason cited automation and AI-enabled systems for operational functions in an earnings call at the beginning of the year.

In January, the CEO of Bank of America Brian Moynihan wrote in the bank’s annual report that AI “saves us about 2,000 people” who would otherwise write code. In an investor’s meeting in February, JPMorgan Chase CEO Jamie Dimon said that “there’ll be fewer jobs in certain functions.”

At the same time, the very same institutions are racing to deploy artificial intelligence. JPMorgan now has over 200,000 employees using its in-house AI tool, according to a 2025 earnings report. It projects operation teams will be more than 40% more productive than 2025 levels within five years thanks to AI.

Bank of America reached 90% of adoption in April 2025, the company said last year. Morgan Stanley hit 98% among its financial advisors, the bank announced in 2024.

“We’re talking about a level of scale that is candidly unprecedented,” Goldman Sachs CEO David Solomon told investors in 2024.

Some call it a revolution, others a “modern gold rush” accompanied by a boom in productivity and corporate earnings. Mostly, it fuels an unstoppable surge in valuations, all justified by bets on the future rather than current earnings.

Some call it a revolution, others a modern gold rush. Finance CEOs are hinting at sweeping disruption. Optimists, like Nvidia CEO Jensen Huang, argue at the May 2026 Milken conference that AI will change the kinds of tasks workers do and create more jobs than it eliminates. Pessimists disagree. Anthropic CEO Dario Amodei predicted in an Axios interview that AI could wipe out half of all entry-level white collar jobs within five years.

Amid the noise, it is worth stepping back and looking at the numbers. So far, there is more speculation than measurable change. In a moment already muddied by post-Covid turbulence, rising geopolitical tensions and shifting interest rates, conflating noise with signal carries a real cost for workers trying to make sense of their futures.

“If you’re investing in AI and it’s unclear whether the productivity effects are there yet but you want to do these layoffs anyway, then AI seems like a good excuse for doing so,” said Anders Humlum, an economist at the University of Chicago Booth School of Business studying how AI affects workers and firms. “One should be very careful looking at the trends and then ascribing them to AI, it’s not the only thing going on in the world.”

First, the adoption data

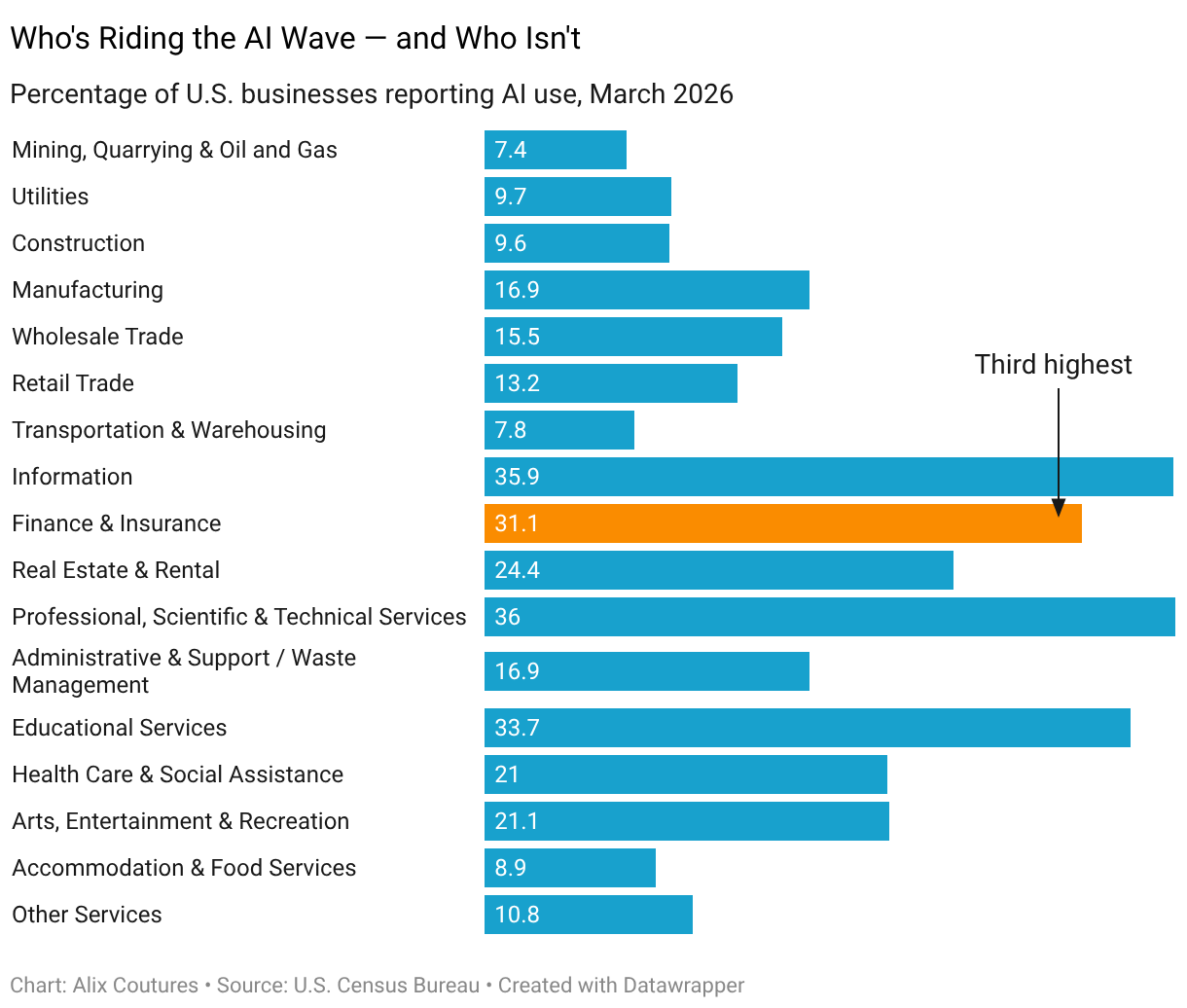

Finance and insurance is among the highest AI-adopting industries in the country, with 31.1% of companies reporting use in March 2026, according to the U.S. Census Bureau, which tracks adoption biweekly.

In banking, Goldman Sachs rolled out an internal AI assistant for summarizing documents, drafting content and analyzing data. “It’s like the ultimate librarian that knows how to find information,” CIO Marco Argenti said in October.

JPMorgan Chase’s AI suite, used by over 200,000 employees worldwide, covers fraud detection, customer personalization, pricing and software development, the company said in a letter to shareholders. Bank of America’s virtual assistant Erica handles hundreds of millions of customer inquiries a year.

In insurance, Travelers announced in a 2025 earnings call that more than half of incoming calls were eligible for AI processing, including a generative AI voice agent handling first notice of loss by phone.

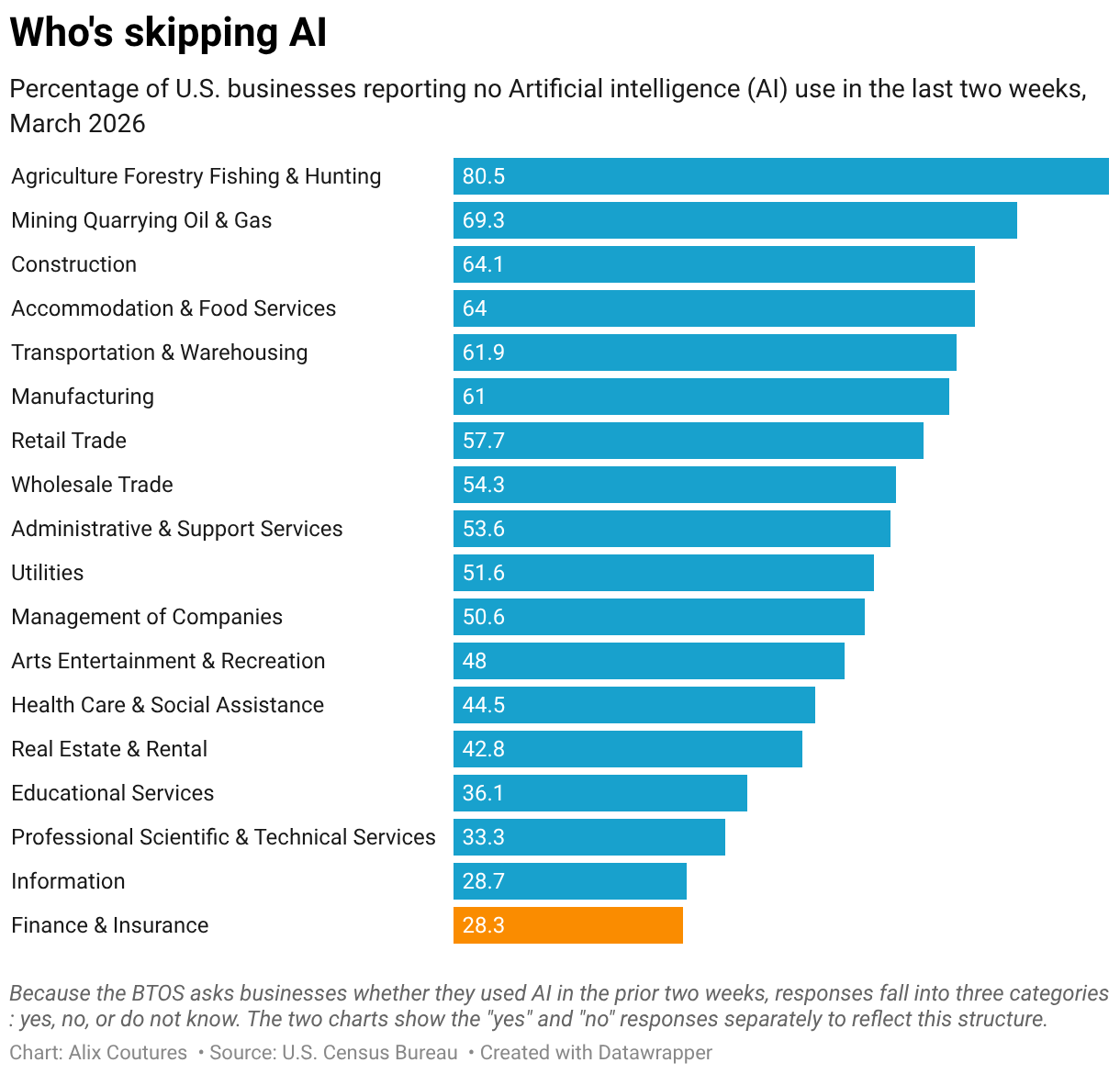

Adoption is not universal, however. In the same Census survey, 28.3% of finance and insurance companies reported not having used AI in the past two weeks. “Many firms were not even allowing those tools to be used because of data confidentiality,” said Humlum. “Most workers and firms are still trying to figure out how to best use these tools.”

What does it mean for productivity?

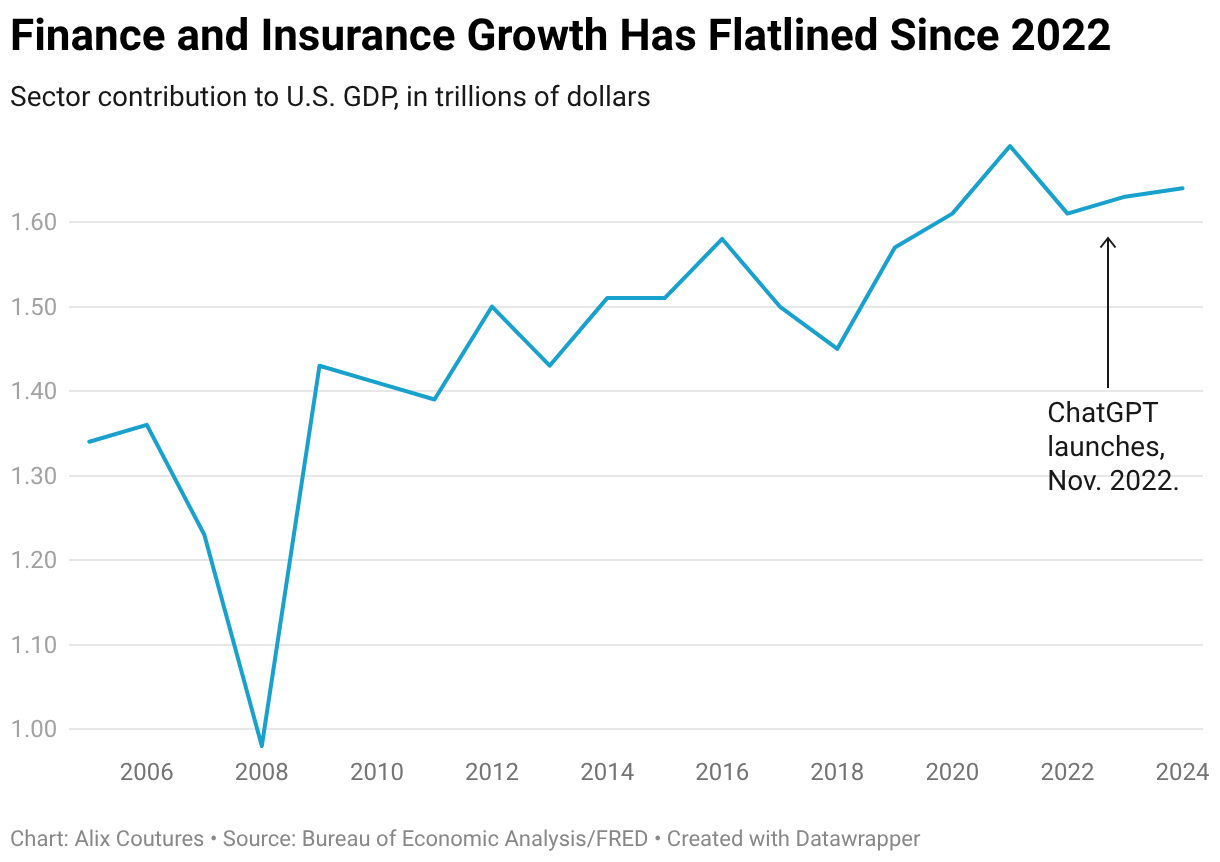

Despite bullish predictions from executives, AI gains have not yet shown up in the data. In 2024, the sector’s contribution to U.S. GDP was $1.64 trillion, up only slightly from $1.61 trillion in 2022, when ChatGPT launched, and still below the $1.69 trillion peak of 2021.

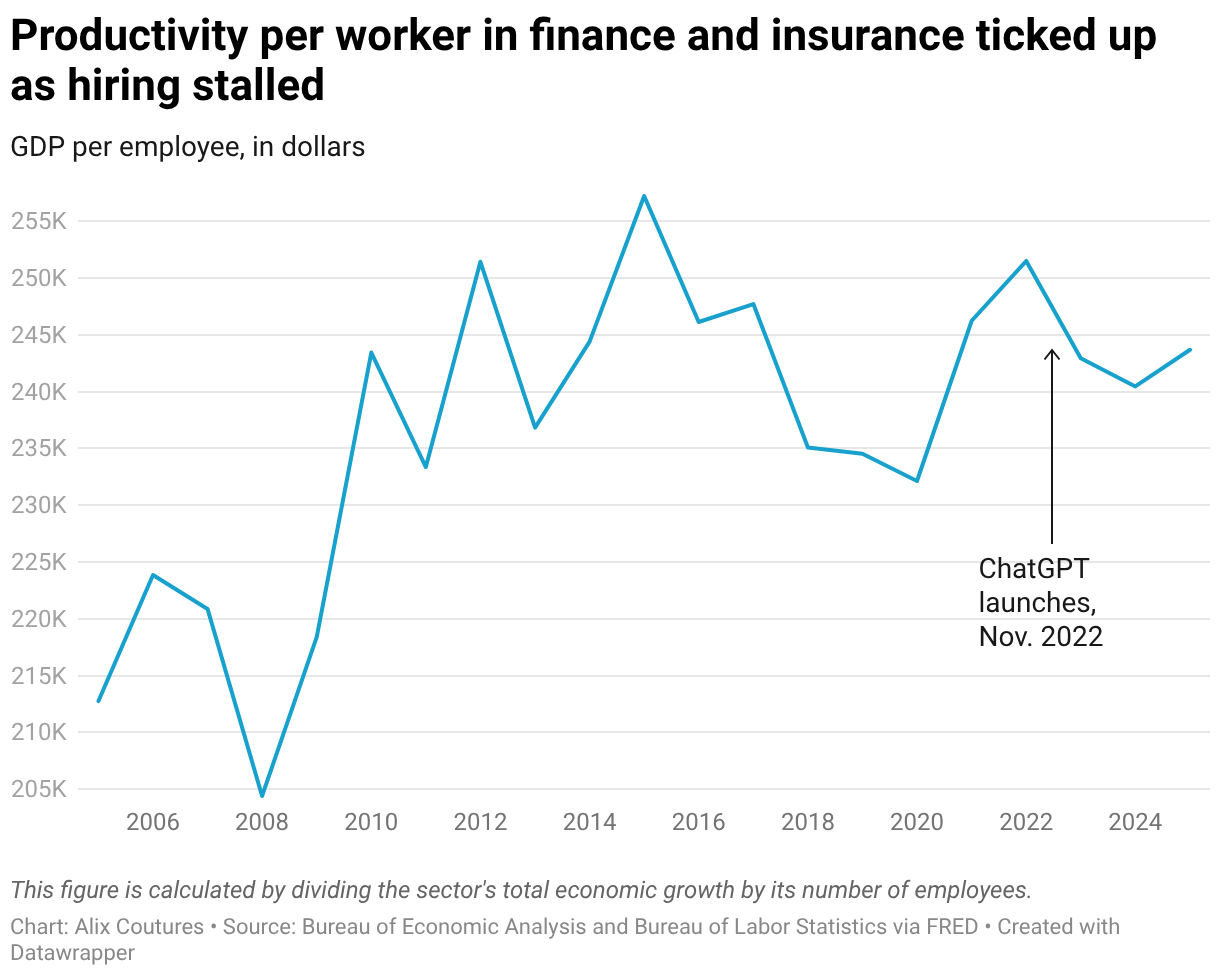

Productivity per worker tells a slightly different story. Calculated by dividing total economic output by the number of employees, it stood at $244,000 in 2024, up from $232,000 in 2020.

But Humlum cautions against reading too much into that rise. Companies shedding excess pandemic hires would mechanically push the number higher, with no AI required.

“It takes a while for those technological improvements to show up in the productivity data,” said Ryan Nunn, Director of Research at the Yale Budget Lab, which tracks the impact of AI on the labor market. “The LLMs themselves have gotten so much more powerful just in the last months, and businesses are still in experimentation mode.”

Olivier Toubia, a professor at Columbia Business School specializing in innovation, offers a structural explanation. If every firm adopts AI simultaneously, no one gains a competitive edge, and prices do not rise.

“AI can make us more productive but it doesn’t necessarily make us more competitive in the market,” he said. “The products are better but customers don’t necessarily pay more because there’s no clear differentiation.”

What about employment?

Companies are announcing sweeping layoffs. But are they actually cutting headcount or performing for investors?

The picture is uneven. Citigroup, Bank of America and HSBC show modest declines in headcount. Citigroup counted approximately 226,000 employees in 2025, down from 240,000 in 2022. But JPMorgan has surged to 318,000, while Goldman Sachs and Morgan Stanley remained flat.

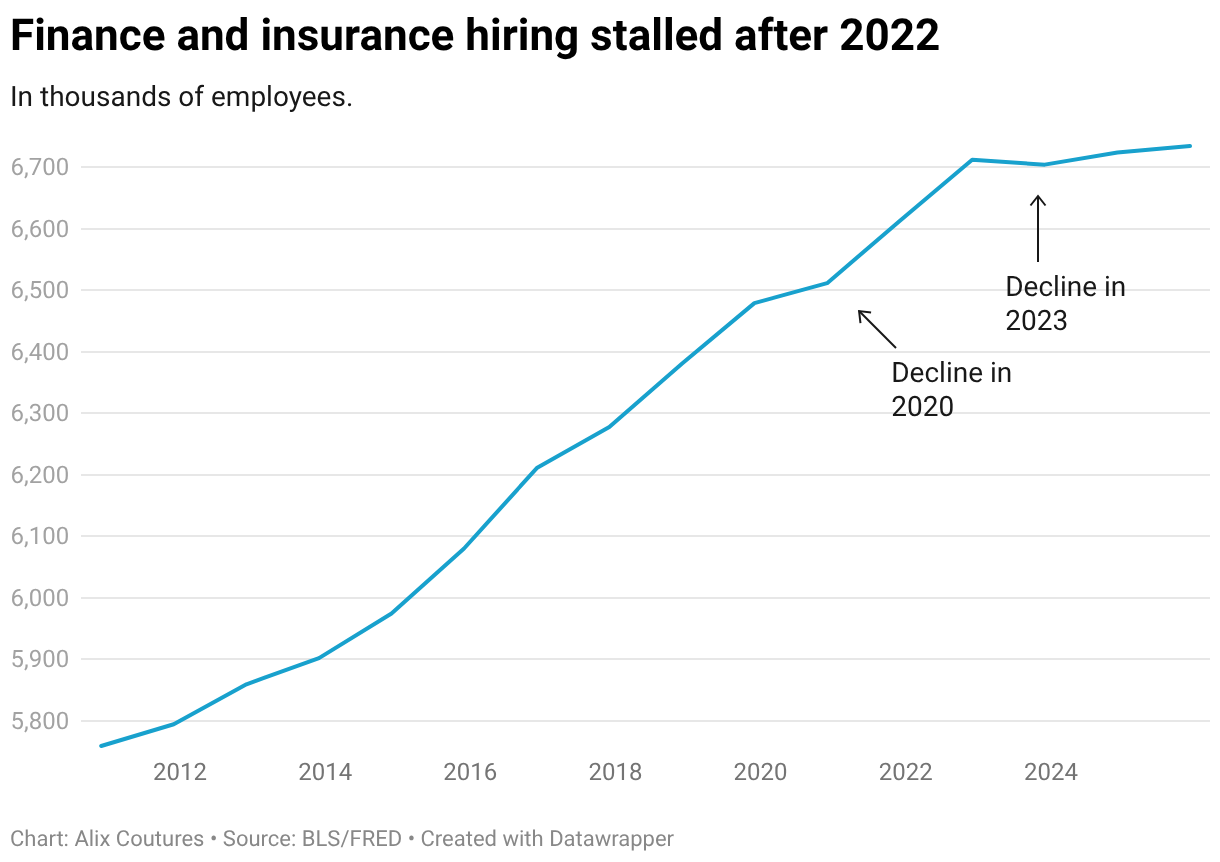

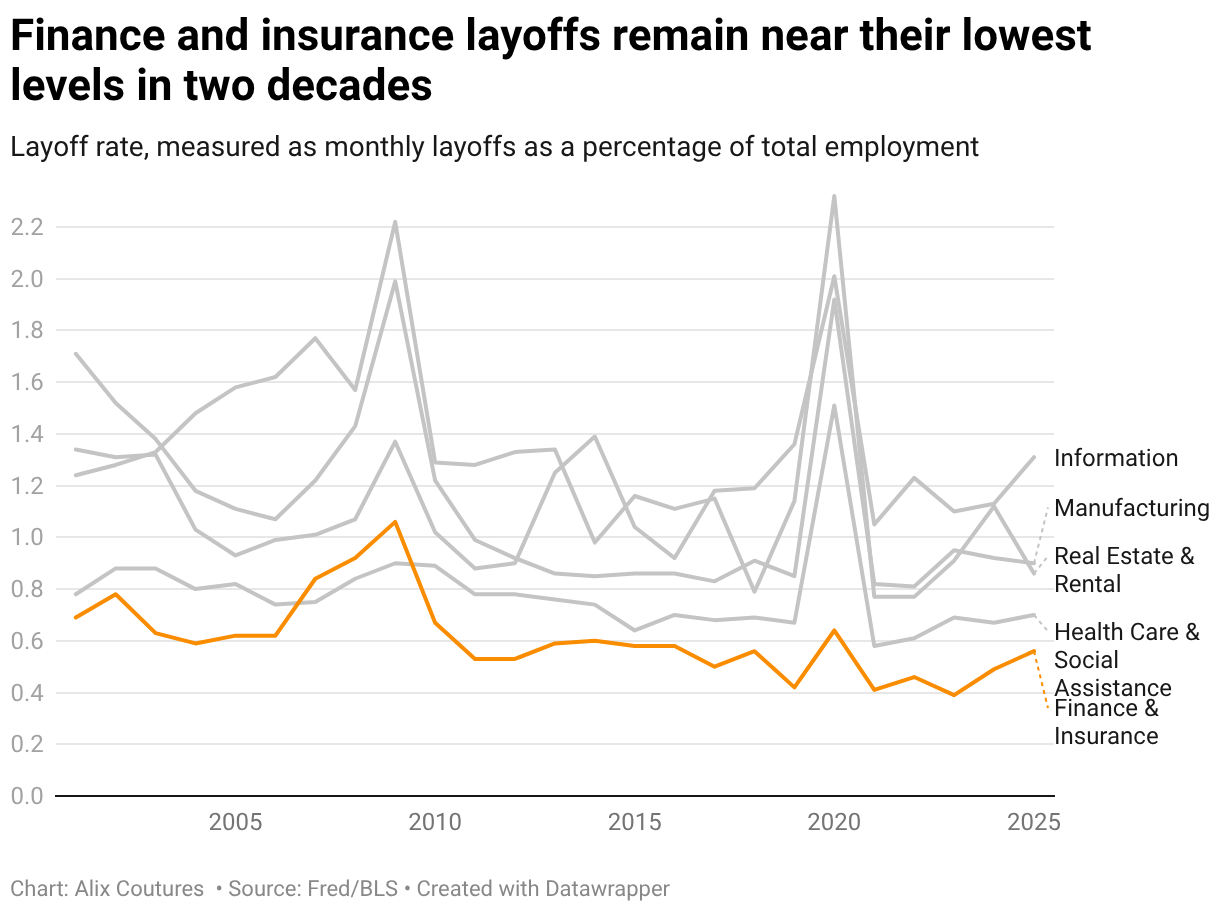

Overall, hiring has stalled while layoffs have stayed very low, at a 0.56% rate in 2025 in a low-hiring – low-firing environment.

“We do not have strong evidence that the labor market is being disrupted right now,” said Nunn. “Unemployment is distributed in pretty much the same way it was before AI.”

Some announced layoffs may be cover for pandemic overhiring, weaker product demand, or simply investor relations strategy, rebranded as AI restructuring. The headcount picture may also reflect a balancing act between roles eliminated and new ones created.

“Companies want to recruit and retain talent to differentiate themselves in the age of AI,” said Toubia. “They could let go of some employees while hiring data scientists. “

Other forces are muddying the picture further. The Fed’s three rate cuts in 2024 supported hiring broadly. And many remote-friendly jobs overlap heavily with AI-exposed ones, making it harder to separate the effects of return-to-office mandates from those of automation.

Rather than replacing workers, AI could yet create more jobs. Torsten Slok, economist at Apollo Global Management, predicts a boom in both productivity and employment. “When things get cheaper, demand goes up,” he wrote in an April newsletter. “When the cost of professional work falls, the addressable market expands and the total number of firms and workers in the field grows.” He points to the steam engine: Britain didn’t burn less coal after it became more efficient, it burned more.

The same pattern is happening right now with radiologists. Often cited as the most vulnerable to AI, the field is seeing a surge in demand. As impressive AI tools emerged, specialists were predicting mass job replacement. “People should stop training radiologists now,” Geoffrey Hinton, computer scientist and Turing Award winner said in 2016.

Yet, the demand has never been higher. Several reasons for that: models are trained on narrow data sets, autonomous tools face a high regulatory bar and radiologists are still needed for communication, oversight and teaching.

Also, as AI makes imaging faster and cheaper, demand for scans increases, keeping radiologists busy.

In the Finance and Insurance sector, it is still too early to draw conclusions. Humlum estimates slight changes could appear within two to three years, with full impact taking closer to a decade.

“I’m sure these tools will be super transformative in the long run and will show up in productivity statistics,” he said. “We just probably haven’t driven off a cliff yet.”